{kind=link}

India’s Poultry Sector in FY 2024-25: Demand-Supply Dynamics and Growth Outlook

DR K. RAVI, SCIENTIST,CARI

The Indian poultry industry continues its robust expansion, with the market size reaching approximately INR 2,304 billion in 2024, and is projected to grow at a CAGR of 12.6% to touch INR 8,430 billion by 2033.This growth is fueled by rising urban incomes, evolving dietary preferences favoring protein-rich foods, and increased demand from the food service sector.

Demand and Supply Trends

- Revenue Surge: The sector saw a revenue increase of over 30% in FY 2022-23, driven by higher realizations and steady volumes.

- Broiler Meat Prices: Broiler chicken prices averaged Rs. 135–140 per kg in FY 2022-23, with continued upward pressure due to strong demand from the HORECA segment.

- Feed Cost Inflation: Prices of maize and soymeal—key poultry feed ingredients—rose by ~35%, squeezing margins for producers. These elevated costs are expected to persist through FY 2024-25.

- Production Expansion: Poultry production expanded by 12% in FY 2022-23, with new capacities expected to come online in early FY 2024-25 due to short setup timelines of 3–6 months

Sector Performance and Efficiency Gains

- Livestock Sector Growth: From FY 2015-16 to FY 2020-21, the livestock sector registered a CAGR of 8%, with poultry leading the charge.

- Egg Production: Egg output grew at a CAGR of 7.6%, reaching 120 billion units by FY 2021.

- Efficiency Improvements:

- Feed Conversion Ratio (FCR) in broiler production improved to 1.55–1.6, down from 1.8–1.9 a decade ago.

- Layer birds now produce 330 edible eggs during their economic lifecycle.

- Breeder birds yield ~180 hatching eggs over 68–70 weeks.

Market Outlook and Structural Shifts

- Projected Growth: The poultry sector is expected to reach USD 35 billion in the next five years, supported by demographic shifts and increased protein consumption

- Organizational Maturity: The industry is becoming more structured, with integrated cold chain logistics and digital supply chain systems gaining traction, especially among Tier 1 and Tier 2 suppliers

- Global Alignment: India’s market is mirroring global trends, with a gradual shift toward white meat and increased export demand, partly driven by bird flu outbreaks in other countries

Socioeconomic Impact

- Employment Generation: The sector provides direct and indirect employment to over 5 million people, contributing 5% to India’s agricultural GDP.

- Rural Empowerment: Poultry farming continues to be a vital source of livelihood in both rural and semi-urban regions.

The Indian poultry sector stands at a pivotal juncture, balancing high demand with supply-side constraints. With strategic investments in infrastructure, feed efficiency, and digital integration, the industry is poised for sustained growth and deeper global integration.

Despite branding efforts, over 90% of poultry products in India are still sold in undifferentiated wet markets, creating intense price-based competition.

In recent years, the Indian poultry industry has made notable strides in brand development and value addition, particularly in processed chicken meat and packaged eggs. These efforts reflect a growing awareness of consumer preferences for hygiene, traceability, and convenience. However, the sector remains predominantly commoditized, with approximately 91% of poultry meat and eggs still distributed through traditional wet markets and open wholesale channels .

This market structure closely resembles a perfect competition scenario, where products are largely undifferentiated and price becomes the primary—often the only—basis for consumer choice. In such an environment, poultry farmers face significant pressure to match or undercut competitors’ prices, regardless of their operational efficiencies or product quality. This dynamic frequently leads to underpricing, eroding margins and exposing producers to financial stress.

Despite improvements in production metrics—such as feed conversion ratios and egg yield per bird—many farmers struggle to capitalize on these gains due to the lack of market segmentation and brand recognition. The absence of cold chain infrastructure and limited penetration of organized retail further reinforce the dominance of live bird sales, which restrict shelf life and inhibit value-added offerings .

To break free from this cycle, the industry must accelerate its shift toward organized retail, integrated supply chains, and consumer education. Encouraging adoption of processed and packaged poultry products, supported by robust branding and certification standards, can help producers differentiate their offerings and command premium pricing. Additionally, policy support for cold chain development and incentives for small-scale processors could catalyze this transformation.

As India’s poultry market is projected to grow from INR 2,304 billion in 2024 to INR 8,430 billion by 2033 .the opportunity to reshape its competitive landscape is immense. Strategic investments in infrastructure, marketing, and digital platforms will be key to unlocking sustainable profitability for producers and delivering safer, higher-quality products to consumers.

India’s Poultry Sector: Evolving Demand-Supply Economics and Strategic Imperatives for Sustainable Growth

India’s poultry industry is undergoing a transformative phase, marked by rising consumer demand, evolving market structures, and critical supply-side challenges. As of FY 2024, the sector has reached a market size of INR 2,304 billion, with projections indicating growth to INR 8,430 billion by 2033, driven by increasing urbanization, changing dietary preferences, and expanding food service channels

Demand-Supply Dynamics and Price Sensitivity

In a market where 91% of poultry products are sold through wet markets and open wholesale channels, price remains the dominant differentiator. This creates a perfect competition scenario, where producers often sell below cost due to lack of market intelligence, leading to deadweight loss and erosion of producer surplus.

- Consumer surplus arises when intermediaries purchase poultry at prices lower than consumers’ willingness to pay, benefiting from producers’ limited access to retail-level demand data.

- Producer surplus is constrained by price ceilings in undifferentiated markets, despite improvements in production efficiency.

- Opportunity cost is significant, as producers miss out on higher-margin alternatives due to limited integration and market access.

To address this, predictive demand modeling must evolve into actual demand tracking through digital platforms, retail partnerships, and direct-to-consumer channels.

Feed Challenges and Cost Pressures

Feed constitutes 65–70% of poultry production costs, and volatility in maize and soymeal prices has severely impacted profitability. In the past two years, feed prices surged by 35%, with no significant relief expected in the short term .

Strategic recommendations include:

- Government support for importing raw soybean and DDG (Dried Distillers Grain) to stabilize feed supply.

- Trade policy reforms to allow conditional imports under ‘actual user’ clauses.

- Industry-led backward integration through contract farming and partnerships with Farmer Producer Organizations (FPOs).

Economic Framework and Market Intelligence

To optimize pricing and production, poultry stakeholders must embrace microeconomic principles:

- Demand curve analysis to identify optimal price points.

- Consumer segmentation based on age, income, and dietary habits.

- Real-time data on consumption patterns to reduce mismatch between supply and demand.

India’s demographic profile—where over 75% of the population consumes non-vegetarian food and 65% resides in rural areas—requires tailored strategies. While per capita availability stands at 5 kg of chicken meat and 65 eggs, actual consumption among target groups is higher, indicating untapped demand potential.

Policy and Industry Action Plan

To ensure sustainable growth, a collaborative roadmap is essential:

- Government: Facilitate feed imports, incentivize cold chain infrastructure, and support research in poultry nutrition and health.

- Industry: Invest in processing capacity, adopt risk management tools like forward contracts, and build commercial intelligence units.

- Research Institutions: Develop predictive models, track global feed trends, and promote best practices in animal welfare and food safety.

Vision for 2030

By 2030, India’s poultry sector must aim for:

- Integrated supply chains with minimal intermediary leakage.

- Digital demand tracking to inform production cycles.

- Sustainability-driven growth, balancing profitability with nutrition security and environmental stewardship.

With strategic alignment across stakeholders, India’s poultry industry can transition from a commodity-driven market to a value-added, consumer-centric ecosystem.

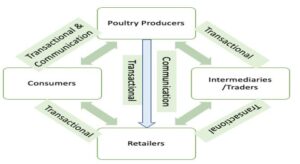

Fig: Traditional Value chain of a poultry Production Cycle:

The Perfect competition in Poultry:

In the recent years, the Indian poultry sector has advanced significantly towards brand building and value addition of chicken meat and eggs. However, the fact of the matter is, about 91% of chicken meat and eggs in the market is still being sold through wet market and open wholesale market as a commodity in a perfect competition scenario. Under such circumstances, the price becomes the only differentiations between the products. Therefore, the poultry farmers are most often compelled to fall into trap of competition from fellow producers and sell their produced at a under-price and incur losses in spite of the performance efficiencies.

Fig: Fundamental Components of a perfect competition environment

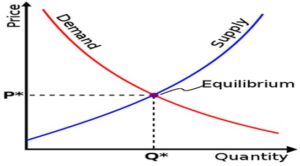

Demand & Supply in Poultry sector:

In this article, an attempt has been made to discuss a few key aspects of demand and supply which applies to the all-range poultry products. Fundamentally, when the demand matches the supply, the price optimises, but in the sectors like poultry wherein the supply and demand data are not available in secondary sources, demand is predicted on the available produced based on a given price.

Fig: Traditional demand and supply Curve with optimal price point

Fig: Illustration of demand curve shifting leading to consumer surplus

Fig: Schematic representation of consumer and producer surplus and Deadweight loss

Opportunity Cost:

Opportunity costs represent the potential benefits that a poultry producer misses out on when choosing one alternative over another. Because opportunity costs are unseen by definition, they can easily be overlooked. Understanding the potential missed opportunities when a poultry farmer or a producer company chooses one options over another allows for better decision making.

Demand Measurement: Predictive Demand Vs Actual Demand

Sources: Statista 2022

Segmentation of Consumers:

Table: Illustration of Indian population DemographyTable: Illustration of Availability of Chicken meat and eggs on target Population

Fig: Demand Measurement tools

Fig: Schematic representation of desired relationship framework among the stake holders